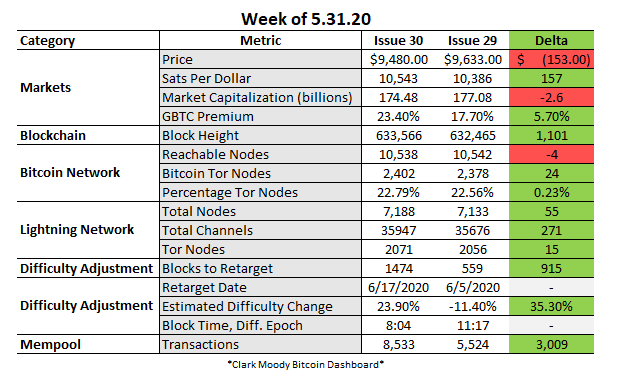

Week of 5.31.20 - Issue #30

Hi friends,

Welcome to the 30th edition of the ₿it Economy! Feedback and suggestions are very welcome, especially from the new folks. Every week I write a blurb about something I learned that's broadly Bitcoin related. If you have thoughts, I'd love to hear from you. My goal is to shed a tidbit of info that I believe will get you thinking about the digital world around you. If you know anyone who would be interested in the topic, please do forward this along, send them to archive, or have them subscribe here.

-Rob

TLDR

Another wild week in Bitcoin that saw the price cross the psychological barrier of $10,000 only to have it drop back down to $9,600 the following day. Yet, as much as people would like to discuss price there is a more important topic — privacy. In response to protests around the world, governments have stepped up their surveillance on its citizens. It’s too soon to know the granular details on what tools these organizations but we can assume that there are a lot of them — contact tracing apps, facial recognition tools and drones to name a few. But one that often slips the mind is the use of credit and debit cards. Buy something online? Pay with plastic. Heading to a chic coffee shop? Insert chip here. Sending friends money for food? Just Venmo me. The ever-evolving demand for convenience has given rise to a slew of life simplifying products. So what is next in the crosshairs? Cash.

The Race Towards CBDCs & the War on Cash

Key Takeaways:

Central banks around the world are exploring the implementation of digital currencies.

CBDCs rely on blockchain technology and aim to replace the cash in circulation.

Both Facebook and the PBoC have made significant headway with CBDCs

A cashless society allowed the administers of CBDCs to analyze its citizen's transactional data.

Bitcoin as a non-sovereign digital currency offers users a way to circumnavigate the surveillant nature of CBDCs.

Around the world, central banks are flirting with digital currency. As the coronavirus threatens the existence of cash, some 40-something countries have either drawn up plans or begun the development of some version of a central bank digital currency (CBDC). There was even a mention of a Digital Dollar to distribute those whopping $1,200 Trump Bucks you may or may not have received in April.

CBDC is going to be a trending topic for years to come, and it is important for the masses to have an understanding of the good, the bad and the ugly. Below, I set out to provide you with their origin story, explore the examples and explain how they could impact cash and ultimately Bitcoin.

So what is a CBDC?

CBDC is, simply put, digitized cash — therefore a secure digital equivalent of a paper bill that can be used for payments, store of value and a unit of account. Much like a traditional currency bill that carries a unique serial number, each CBDC unit will be distinguishable to prevent imitation. You can think of it as cash in circulation as it is intended to replace paper notes with a form of digital cash that can be directly issued by the nation-state without the necessity of an intermediary.

The common denominator between CBDCs and other digital assets like Bitcoin is that they both rely on the underlying blockchain technology — a digital ledger that allows transactions to be recorded and accessed in real-time. As a part of the money supply controlled by the central bank, it will work alongside other forms of regulated money, like coins, bills, and bonds. A few of the potential benefits of issuing a CBDC include:

Decrease the cost of issuing new cash (no money printer go brrrr)

Improve financial inclusion

Decrease transaction, settlement and reconciliation costs

So now that we have some background, let's explore a few of the big players looking to seize the opportunity.

Facebook Takes a Stab

In June of 2019, Facebook publicly announced that they had been working on a digital asset project, named Libra. The idea was an innovative one — a consortium of global corporations that would be responsible for creating a global digital currency that revolutionized the way money moves across borders. Yet, when considering cross border payments, they are understandably complex.

Say for example you would like to send a payment from the U.S. to China. For starts, you will need to employ the service of a correspondent bank and the multiple requirements that come with it. This burdensome process often takes 2-4 business days where Libra would cut the time down to almost instantaneously.

So far so good right? Well... keep in mind this is Facebook who we are dealing with. To the dismay of the social media giant, its proposal was met with significant pushback from central banks around the globe. So much that as of March 3, 2020, Facebook no longer intends to make the Libra token the centerpiece of its digital strategy. Rather, it has succumbed to political pressure and will transition to supporting both existing government-backed currencies, like the US dollar and the euro, and then the Libra token when it is eventually completed and ready to launch (doubtful).

China Seeks Control

As Facebook's Libra flounders, the world's second-largest economy has now taken center stage when it announced its intention to develop a Digital Yuan. Back in August of 2019, the Chinese Government's central Committee issued a white paper titled Opinions on Supporting Shenzhen's Pioneering Demonstration Zone with Chinese Characteristics.

It mentioned that by "seeking to build a modern economic system that reflects the requirements of high-quality development, it supports the development of innovative, future-minded applications such as digital currency research and mobile payments."

Hundreds of millions of people in the People's Republic of China have already shifted away from cash to using smartphone apps such as WeChat and Alipay. Therefore it is no surprise that a CBDC is the next step in China's plan to develop a fully-fledged digital nation.

While the Chinese central bank believes the digital version of the fiat currency would give its people the ability to be a part of the new digital economy, it raises questions with what will happen to all that data.

As the nation steamrolls ahead with the launch of its digital currency, it would more than likely have all the monetary tools in place to create a closed-loop surveillance state. With a completely state-sanctioned digital currency, one where paper money and metal coins are done away with, all purchases and transactions, including the time and place where they occurred, can be tracked analyzed, judged and prosecuted — instantaneously.

The Anti-Cash Movement

In recent years, numerous businesses have made headlines for refusing to accept cash as a form of payment. These businesses span a variety of industries, including airlines, eateries, sports stadiums and coffee shops. In behavior economics, this is referred to as "nudging". If a powerful institution wants to make people choose a certain thing, the best strategy is to make it difficult to choose the alternative. The objective is to reverse-engineer a belief within oneself that it is inconvenient, and that a cashless society is in my best interest.

Well, it is quite the opposite. A cashless society is in the best interest of banks and payment companies. A cashless society brings dangers. It consolidates and expands the power of the banking system who simultaneously bundles up your transactional data to sell it to the highest bidder.

Cash is in fact the only form of money we can physically hold. Many forget that on every U.S. Dollar it says "This Note Is Legal Tender For All Debts, Public and Private."

The money that we see in our bank accounts is actually an IOU. Banks create their own money in the form of deposits, denominated in a nation's money of account. A deposit is a bank's IOU to convert bank money into currency (government money) at a deposit holder's request. Therefore, every time you or I go to the ATM and take out cash, we are exiting the banking system (and therefore the surveillance that comes with it). The payments industry does not have insight into what you or I spent our cash on. One of the most important qualities of true cash is that it can be anonymously transferred between entities. That fundamental level of privacy is imperative to keep as we advance into this decade.

Unfortunately, due to the coronavirus pandemic, that fundamental level of privacy day's are numbered. There is blood in the water and the payments industry was the first to jump at the opportunity with central banks not too far behind. As each day goes by, paper cash is being eliminated as a tool for those who do not want their location and identity tracked and aggregated alongside their personal data. However, the creation of digital assets like Bitcoin offers users a potential opt-out.

Impact on Bitcoin

While it has yet to be seen, a case could be made that CBDCs may act as a gateway for more retail and institutional interest in Bitcoin. The very existence of CBDCs strengthens the case for non-sovereign digital currencies, like Bitcoin. It was invented to transcend borders free of government control and operate outside of the traditional banking system. If governments want to do the heavy lifting, by all means, the ecosystem would be happy to let them. Onboarding billions with digital wallets and getting them familiar with digital currencies can only be positive.

What is Next?

Central banks play a pivotal role in the economy in the form of monetary policy. As every day goes by, the monetary policy is becoming increasingly difficult as financial markets become exceedingly complex. The idea of a cashless society is no longer an imaginary concept and the coronavirus may have been the nail in the coffin. However, as governments around the world unveil their respective CBDCs, they will onboard billions of users to digital currencies. It is only a matter of time that they become interested in Bitcoin.

News 📰

S1: Square Crypto Announces 6th Development Grant

What is it? - By now you all should be familiar with Square Crypto — Bitcoin development initiative of Jack Dorsey led Square. On Monday, the firm announced that it will be awarding its 6th development grant to Segi Delgado and Talaia Labs, for his work on The Eye of Satoshi — a FOSS Lightning Network watchtower. A watchtower is a third party lightning node, that can detect if a dishonest party attempts to steal funds and then broadcast a justice transaction, sending the funds back to the honest party, even if or when that respective honest node is offline. Basically it is a way to ensure peers can't close the channel and run off with your bitcoin.

Bonus - Check out Sergi Delgado speak on Potzblitz last week. Warning this is an hour long 😃

Why it Matters? - Back in March, I covered BitMEX and the exchange's decision to increase Michael Fords (aka fanquake) Core Developer Grant and the importance of funding further development.

Free and Open Source Software (FOSS) is critical to building trust and safety into the Bitcoin network. Bitcoin is disruptive, just as Apple disrupted mobile phones, Tesla disrupted automotive, and Twitter disrupted media and commutation.

The Bitcoin network is used by millions of people around the globe on a daily basis. Many rely on the base layer infrastructure to power applications and transfer wealth across borders. But without developers, there is no technological breakthrough. Thankfully, companies like Square Crypto, among others, are awarding developers grants (and opportunities) to build unique solutions to the protocol. To date, the initiative has provided six grants listed below:

As Bitcoin continues to grow it may one day become a large member of the geopolitical stage. At that point, there may be many traditional companies that contribute to the protocol through various avenues. In April, after news of a16z's $515 million crypto fund, I raised the question that venture capital firms who dabbled in crypto should allocate a minor portion of their fund to open source development. Citing that it may be easy to lose sight of the fact that Bitcoin is a multibillion-dollar industry, that some of its portfolio companies (e.g., Coinbase and Anchorage) rely on.

I am well aware of the fiduciary responsibilities that VC's have to their LPs but I am positive that some of the greatest minds in the space can get creative with their capital allocation. As this asset class continues to evolve, one thing is clear — there cannot be just a handful of digital asset focused companies and even less publicly traded companies willing to spend to build the infrastructure that is the heart of this entire ecosystem.

Final Take - For Bitcoin to be successful, everyone must do their part.

Bonus - Further information about the six grants and the link to apply for your own:

Bonus -BitMEX awarded another grant to Bitcoin contributor and researcher Gleb Naumenko.

S2: Avanti Raises a $5M Angel Round

What is it? - Avanti Financial Group Inc. is a Wyoming corporation headed up by Caitlin Long — long time bitcoin and blockchain policy advocate for the state of Wyoming. Earlier this week, the firm announced that it had raised a $5 million angel round. Funding was led by the University of Washington Foundation with participation from Morgan Creek Digital, Blockchain Capital, Digital Currency Group, Lemniscap, Madison Paige Ventures, Malex Enterprises, Susan B. Anthony, LLC and others.

Why It Matters? - A couple months back, this newsletter mentioned that Avanti Bank intended to apply for a bank charter under Wyoming's special-purpose depository institution (SPDI) law. The bank previously raised a $1 million seed and with new funding secured, Caitlin and fellow team now have the capital to navigate the application process. Instead of replicating the traditional creditor and debtor relationship like traditional commercial banks, Avanti plans to employ the state's unique legislation to build a bank aligned with Bitcoin's ethos. And though, there are plans in the pipeline to offer custodial services for security tokens, the work to set up Wyoming as a safe-haven for digital asset native companies cannot be understated. This reflects a broader trend of "Bitcoin-only" focused companies — Swan Bitcoin, River Financial,Fold, Lolli, CoinFloor, BullBitcoin and Amber to name a few.

Final Take - The SPDI is a gateway for institutions both new and preexisting who want to buy Bitcoin without the constant worry of the various risks (e.g., legal and credit) surrounding it.

Bonus - Few of my favorite podcasts sharing more detail on Avanti:

The Pomp Podcast #241 - Coronavirus: The Pin that Popped the Credit Bubble

Unconfirmed #114: How Avanti Will Be a "Not Your Keys, Not Your Coins' Bank

Market Watch 💸

What I'm Reading 📕

57 Varieties of Pyrite: Exchanges Are Now The Enemy of Bitcoin

Coinbase Wants to Sell Blockchain Analysis Software to IRS & DEA

Toxic Recall Attack - Unwinding Joinmarket Case Study

What I'm Listening To 🔊

What I'm Watching 📺

Project Announcements 📢

Project Spotlight 🔦

goTenna

Stage of Funding:

GoTenna has raised a total of $40.8 million in funding over 4 rounds. Their latest funding was raised in June of 2019. Notable investors include Union Square Ventures, Bloomberg Beta and Founders Fund.

Business Model:

GoTenna is a startup focused on connecting users without an internet connection: a mesh network. Essentially a two-way radio for mobile phones that pairs with your device using Bluetooth and uses 151-154 MHz radio to communicate with the outside world. Best known for its outdoors-oriented consumer product that allows users to text and share locations between smartphones of the grid.

Audience:

The Brooklyn-based startup is offering a solution for off-the-grid travelers who need low-cost connectivity for their smartphone. The device can be strapped to a backpack or belt loop and creates a low-frequency radio wave network for mobile phones that can last around 1 mile in skyscraper-filled urban areas, but up to 9 miles in most outdoor situations.

Last year the firm partnered with Blockstream to enable both sending and receiving Bitcoin transactions without an internet connection. The Blockstream Satellite is a network of satellites that broadcast activity based on the Bitcoin network. The combination provides another way Bitcoin users can interact with the network as well as added privacy benefits that centralized services can not offer.

Media:

Final Quote

Thanks for reading. Send me tips, stories I’ve missed, or comment below. And if you liked this piece, you can sign up here for more issues of the Bit Economy, a newsletter on something bitcoin related.

Have a great week! See you next Sunday.

If you liked this post from The ₿it Economy by @rsarrow, why not share it? Use the link below to share on your social media platforms. Want to get in touch? Find time to connect here.