Hi friends,

Welcome to The ₿it Economy! I’m Rob, and each week I write a blurb about something I learned that’s broadly Bitcoin related. First off, a wild end to the week culminating with my birthday is to blame for the delay in sending out Issue #44. I had hoped that by writing the main story at the beginning of last week, I’d be able to package it up for the usual Sunday morning release. Unfortunately, that did not happen and here we are on a Tuesday.

As for more positive news, I’m happy to announce that I'll be joining the research team at Blockchain Capital this fall as a research scholar. Personally, couldn't be more excited to make an impact on a team that has been around since the early days of this industry. That being said, I want to apologize in advance if I miss a week or two of the newsletter.

And of course, if you have thoughts, I'd love to hear from you. My goal is to shed a tidbit of info that I believe will get you thinking about the digital world around you. If you know anyone who would be interested, please do forward this along, send them to the archive, or have them subscribe here. 👇

-Rob

A Trojan Horse

Back in June, I wrote about the COVID-19 pandemic being a trend accelerator towards Central Bank Digital Currencies and the greater war on cash. Now, a few months later, it is becoming evident that 2020 is an inflection point for digital payment adoption in the U.S. As it stands, Bitcoin is the king of the digital asset industry, with a market capitalization of ~$200 billion. It's hands down the most secure network in the world and gives us the opportunity to custody our assets, disintermediate services plagued by middlemen, and engage in dynamic peer-to-peer (P2P) economies.

Bitcoin is still used as a payment method, but it's also seen as a speculative asset and often behaves as such, despite the original intent. As a result, it can be highly volatile, often making it less desirable as a method of payment. On the other hand, stable, predictable valuations support many operations within modern day commerce — recurring payment, loans, credit, savings etc. Thus for those who desire or in need of an alternative, digital asset, look no further than cryptodollars.

Dollars on the Blockchain…

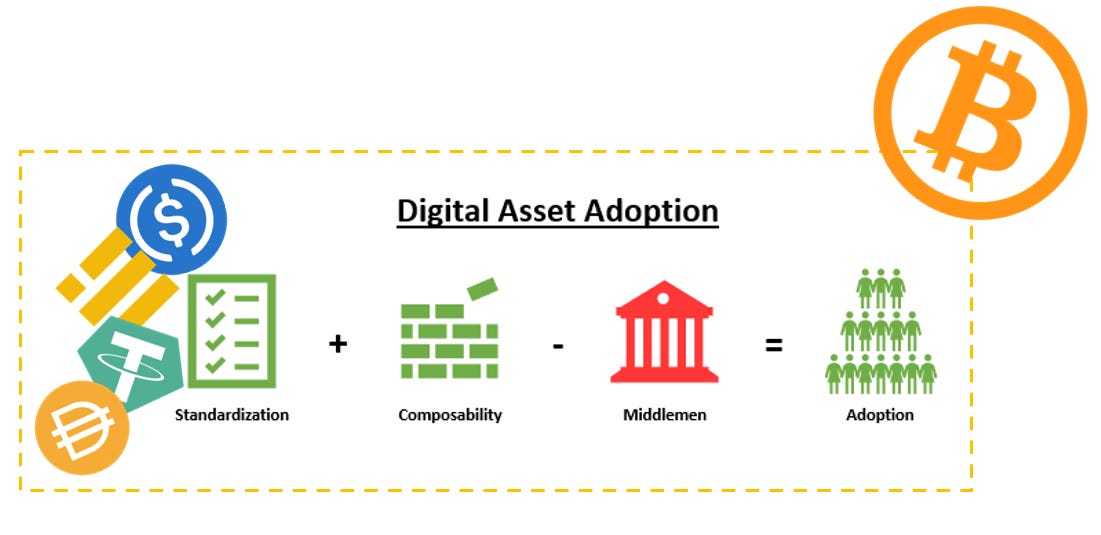

Cryptodollars or commonly known as stablecoins are typically tied to assets like fiat (ex. the US dollar) or gold, giving users the knowledge that the price is pegged to a familiar asset and the ability to hedge against other digital assets. And before some of the people who read this unsubscribe for such Bitcoin blasphemy, just hear me out on this.... cryptodollars are a trojan horse to the masses. Two weeks ago I wrote a simple equation that laid out a path towards Bitcoin adoption.

Humans have always naturally moved towards efficiency. The efficiency accompanies innovation. Cryptodollars are a form of innovation and a core component of standardization in the above equation. People, especially those not tech inclined, are not going to use something that is difficult to understand. So even though you and I know that Bitcoin is a non-sovereign, hardcapped supply, global, immutable, decentralized, digital store of value, all the rest of the 99.98% of the world cares about is being able to pay for a slice of pizza or a fancy cocktail without a hassle.

It was only a few years ago that if you heard the U.S government might mint its own digital currency you'd dismiss the idea completely. But now, central banks around the world are in researching, developing, and launching their own! A frictionless method to transact trade is needed more than ever.

The emergence of central bank digital currencies serves to legitimize and normalize digital currencies as the future of money. We caught a glimpse of this when the “Banking For All Act” slipped its way into the initial drafts of the coronavirus stimulus package. The bill offered a definition for cryptodollars as well as for requirement for all member banks to issue and maintain a user’s digital wallets. And if the distribution of the stimulus checks was any indication, there is a pressing need for a smoother process. For if every citizen had a digital wallet, the currency could be deposited instantly.

Laying Foundation

Earlier last month, the US Office of the Comptroller of the Currency (OCC) issued its second letter granting permission to federally charted banks to custody digital dollar cryptodollars, further opening the door to the mainstream adoption of cryptodollars. Within a broad context, any attention they receive lessens the negative stigmas it has usually been associated with (ex. drugs, tax evasion, etc.). Half of the phycological battle has been won without even doing anything as countries are encouraging their citizens to install digital wallets.

The pandemic has only further pushed institutions down this path. The sustained need for public hygiene at the checkout line, compounded with an astounding demand for simpler ways to shop on-the-go have significantly bolstered core value props of digital payments, most notably via digital wallets and P2P networks. According to a study from Ark Invest, "digital wallet payments grew 41% at a compound annual rate between 2017 and 2019, while those on credit cards increased 13% and those on debit cards, in cash, and by checks declined." As a result, this accelerated shift in consumer behavior will likely further disintermediate consumers from traditional banks and financial service providers, ushering in a more dynamic industry landscape.

Growth

It would be an understatement to say that cryptodollars have seen more adoption in 2020. As of writing, the total market cap for these pegged digital assets sit above $20 billion.

Users can bypass the traditional hurdles of transferring funds and dealing with local currency conversions. So when users of these regulated cryptodollars tire of their limited functionality, lack of privacy, and susceptibility to censorship, they will seek out alternative means of sending money. At this point, they will find Bitcoin and the benefits of an alternative value source that is a gateway to a permissionless financial ecosystem.

Although traditional financial institutions, mobile money and digital assets are districts, there are ways in which they intersect to promote financial inclusion. Cryptodollars fill the current need to transition individuals from the fiat native world to the digital one. We need to learn to walk before we run.

Threads🧵

Breakdown of long-form content that caught my attention

KIN is an Unregistered Securities Offering

News 📰

The top announcements in Bitcoin. All in one place.

BitMEX charged with Violation of the Bank Secrecy Act

NZ tax authority asks local bitcoin exchanges to provide PII

Eye of Satoshi v0.1.1 Released

Chainalysis and Integra FEX win million-dollar IRS contract for Lightning and Monero tracking tools

BTCPay Server v1.0.5.6 Released (Shopify Support)

Bitcoin Wallet Tracker v0.1.5 Released

What I'm Reading 📕

Scowered the internet so you didn’t have to.

Square Valuation Model: Cash App's Potential

Coinbase is a Mission Focused Company

'The Social Dilemma' and The Last Fucking Thing I'll Ever Write About Facebook

What I'm Listening To 🔊

Give your eyes a break and pop in the earbuds.

Creators, Fans, and the Power of Markets

Yield Farming is an Innovation

Using Emotion to Design Great Products

Turning Stranded Energy into Bitcoin

Congressman Davidson, Caitlin Long, and Adam Traidman on Stablecoin

10x Your Bitcoin Security with Multisig

Investing During the Global Crisis

What I'm Watching 📺

Take a break from Netflix and check these out.

Introduction to Schnorr Signatures for Bitcoin & Lightning Network

Governance, DeFi, vAMMs, Layer 2 Solutions

Housekeeping 🏡

Who doesn’t like free money and information?

📅 Subscribe here to stay up to date on early-stage companies building on Bitcoin

🏗️ Aggregated videos, podcasts, news & more from the top Bitcoin startups

🦢Sign up for Swan Bitcoin and receive $10 with your first purchase