Does Your Favorite FinTech Have a Digital Asset Strategy?

Week of 10.18.20 - Issue #45

Hi friends,

Welcome to The ₿it Economy! I’m Rob, and each week I write a blurb about something I learned that’s broadly Bitcoin related. If you have thoughts, I'd love to hear from you. My goal is to shed a tidbit of info that I believe will get you thinking about the digital world around you. If you know anyone who would be interested, please do forward this along, send them to the archive, or have them subscribe here. 👇

-Rob

FinTech's & Their Digital Asset Strategy

In what is arguably the biggest development of the year, financial services giant PayPal announced on Wednesday that it will allow its ~200M U.S. users to buy, sell and store digital assets over the next few weeks. If you feel like you've read this headline before, it's because we first covered this back in June when I said:

PayPal and Venmo combined account for $800 billion in annual payments volume and by offering Bitcoin directly on its platform it would be an incredible boost to not only the digital asset ecosystem but their own bottom lines. Even if 1% of its ~350 million users were to discover Bitcoin on their platform, that would already represent more than 3 million users. That sounds like a small number but it would actually account for ~6% of the total Bitcoin users now.

The news among other factors sent the price of Bitcoin sharply higher as it rose more than 10% to a multiyear high above $13,000. What's more is that the announcement helped send PayPal shares surging 5.5% in the session, finishing the day at $213.07, above their previous closing of $210.82 (Sept. 2nd).

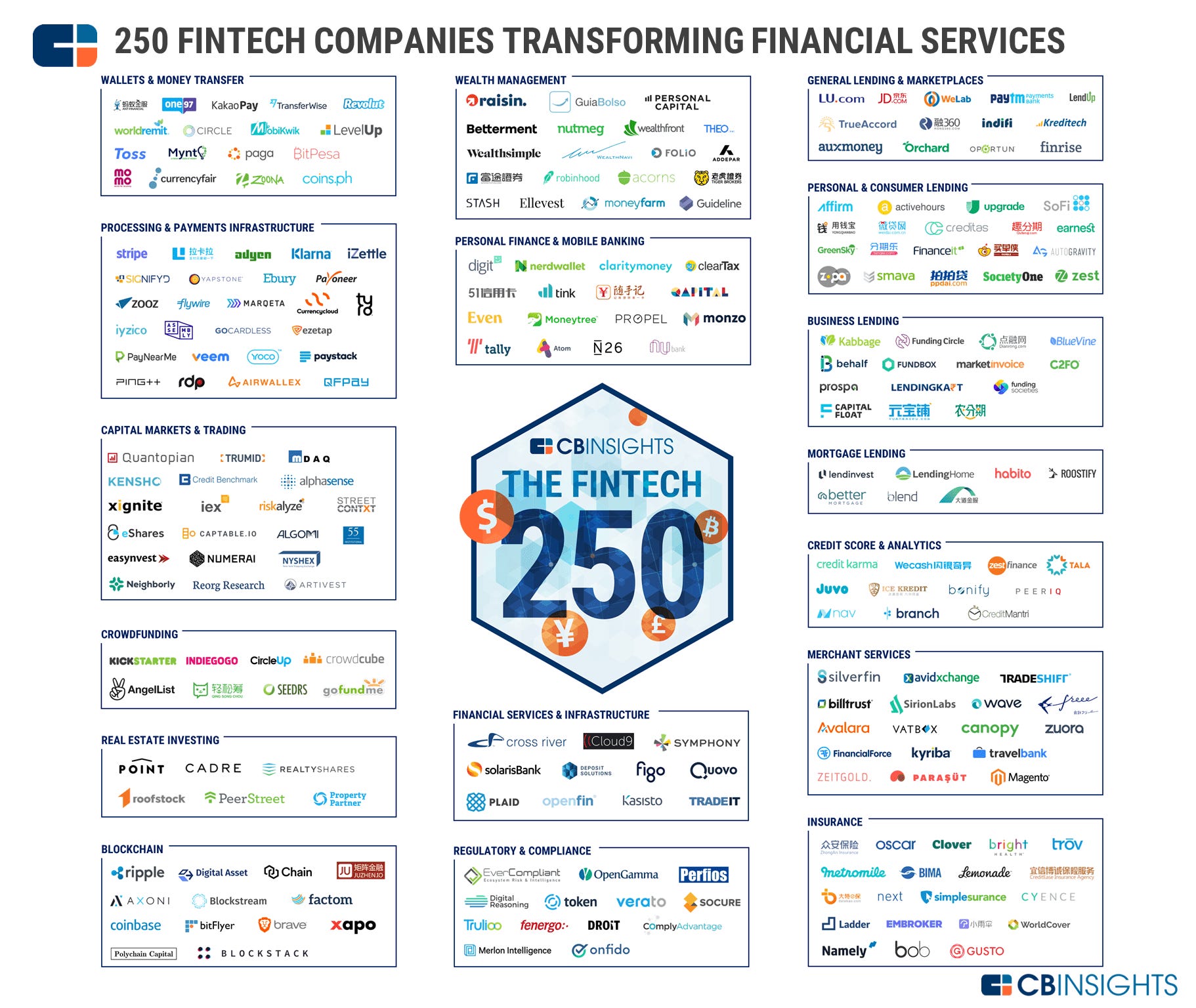

PayPal is a significant business with a market capitalization of $250 billion, a feat that's more than all but three banks in the world. But rather than repeat what's already been said here, here and here — let's take a moment to stop and discuss where the future of payments is heading. Below are 250 of the world's most innovative companies who seek to improve the way you, I and everyone else transact with one another. Of the 250, I'd garner that 20% actually have a digital asset strategy.

Innovation in payments has been the heart of fintech since its inception over 15 years ago. There are multiple components in payments that include mobile, contactless, virtual wallets, voice, identity verification, AI and now digital assets. Mobile payments reached over $1T in 2019. Contactless payments are estimated to hit $760M in 2020. The Neo and challenger banks of the world are making mobile wallets an automatic choice by offering virtual cards to all clients for online purchases and tokenization into Apple, Google, and Samsung Pay (via their smartphone). This transition speaks for itself as Venmo and Square's Cash App have amassed roughly 60 million users organically in the last 10 and 7 years — a milestone that took JPMC more than 30 years and five acquisitions to reach:

We've seen an explosion of intelligent money management apps that consolidate all your accounts in one place (with analytics and alerts) and credit lending apps who have created smarter repayment systems. However, I'd argue that while fintech has disrupted the distribution of incumbents, it has failed to crack the underlying financial infrastructure. While there are teams focused on this, ultimately the core banking systems are underpinned by the likes of SEPA and SWIFT schemes. This is equivalent to throwing a Ford Pinto engine in a Lamborghini's body — sure the outside looks nice but a lot is left to be desired under the hood.

Let's take cross-border payments — the current implementation for servicing global bank transactions is highly complex, requiring them to pay several firms at different levels along the pipeline and it's expensive. It also involves bridging the closed loops of multiple currency systems while often crediting the accounts before settlement.

Enter Digital Assets

In the digital world, financial assets can be used and exchanged with digital assets, which is not tied to a standard currency system. Its online, open-source administration does not require banks or governments for regulation or exchanges, allowing anyone to participate in the system from anywhere in the world.

I wrote a few weeks ago on cryptodollars and their ability to bridge the gap between the traditional world with the open, permissionless and Bitcoin native one. There are use-cases for them in areas like cross-boarder payments and foreign exchange. By pegging a digital asset to a fiat currency like USD has the ability to create a 5-10% yield, opening up an opportunity in the lending-as-a-service ecosystem.

We already have seen this takeoff with centralized exchanges like Coinbase and BlockFi, however, the Cambrian explosion occurred this summer in what many labels decentralized finance (DeFi). If you want to take a loan in the real world, you could take a bank as a counter-party and borrow against it. Whereas DeFi (and Bitcoin) the counter-party is the protocol itself, written as a set of smart contracts on the blockchain. Therefore, despite the inherent risks of new technology, one can see how the products are created and funds are managed.

Digital assets will win over fintech because it is far easier to create new solutions creating and combining new protocols than going through the regulated path of traditional finance. The permissionless and composability properties of this ecosystem allow it to be the perfect short-term complement for its more regulated partner.

Compliments

We have a long way until the world thinks in terms of satoshis. Until then, the role of the fintech incumbents will be to provide its current customer base with a sense of knowledge and security when handling digital assets. The dynamic relationships between banks, fintech and now permissionless protocols have evolved from disruption to collaboration and now towards partnership. Those that understand it is not "us vs. them" and further integrate with these protocols will be rewarded.

With fintech firms pushing into digital assets and central banks openly discussing CBDCs, I would not be surprised to see the world's financial institutions ask their CEOs about their own digital asset strategy during the year-end reviews. Banks, fintech, SMEs, corporates and government all now realize crypto is the biggest thing since the internet and they must adapt. So the question is — do you have a digital asset strategy?

Threads🧵

Breakdown of long-form content into an easy to read and concise format.

Lightning Development is Imperative to the Digital Asset Ecosystem

Bitcoin's Resiliency to Black Swan Events

News 📰

The top announcements in Bitcoin. All in one place.

CME surpasses BitMEX to become second-largest Bitcoin futures exchange

FinCEN fines Bitcoin-mixing CEO $60M

Breez Wallet release candidate

Lightning platform Voltage goes Live

Phoenix Wallet v1.4.0 released

BitMEX to accelerate user verification program

Hodl Hodl announces true P2P lending

Square Crypto awards Riccardo Casatta with developer grant

Market Watch 💸

One-stop-shop Bitcoin market & network snapshot.

What I'm Reading 📕

Scowered the internet so you didn’t have to.

DLC Private Key Management Part 2: The Oracles Private Keys

Bitcoin Optech Newsletter #120

Institutional Digital Asset Ecosystem Q3 2020

The World According to Peter Thiel

The Road to L2 Interoperability

The Two Growth Rates of the Economy

Heat Death: Venture Capital in the 1980s

The Old Radical: How Bitcoin is Being Destroyed

Is There a Credible Bull Case for Ample and Other Elastic Finance Assets?

Audio’s Opportunity and Who Will Capture It

What I'm Listening To 🔊

Give your eyes a break and pop in the earbuds.

The Most Powerful Crypto Trading Platform

A History of America’s Efforts to Shielf Itself from the World

The Paradox of Governance Tokens

Breakout Applications for Web3

The Evolution of Data Architectures

Central Bank Digital Currencies and the Future of Monetary Policy

CFTC Chairman on Crypto Regulation

Should Your Business Hold Bitcoin?

What You Should Know About Bitcoin DLCs

Debt Culture & When Money Destroys Nations

Happiness, Reducing Anxiety, Crypto Stablecoins, and Crypto Strategy

What I'm Watching 📺

Take a break from Netflix and check these out.

Zero Knowledge Proofs vs Fraud Proofs

2020 Virtual Economic Outlook Forecast

Housekeeping 🏡

Who doesn’t like free money and information?

📅 Subscribe here to stay up to date on early-stage companies building on Bitcoin

🏗️ Aggregated videos, podcasts, news & more from the top Bitcoin startups

🦢 Sign up for Swan Bitcoin and receive $10 with your first purchase

Final Quote 🎩

Thanks for reading. Send me tips, stories I’ve missed, or comment below. And if you liked this piece, you can sign up here for more issues of the Bit Economy, a newsletter on something bitcoin related.

Until then, have a great week! See you next Sunday.